Market Overview & Outlook

YTD, Nifty 50 is down more than 10%, and the broader Nifty 500 by ~6%. It has been a difficult start to the year for wealth creation, except for handful of sectors. The narrative hasn't changed much towards India nor has the conviction. The apathy towards Indian equity markets from FPIs have continued and they have been heavy net sellers for all the months in the year barring February. Indian markets have hugely underperformed other Asian markets like Korea and Taiwan, and some of the FPIs exiting India have parked their money there as these markets have been driven by AI themes while there are none in India. To make matters worse, the West Asia war has complicated problems for India which has lowered India's GDP estimates, raised inflation estimates, widened trade and current account deficits and has constrained fiscal deficits.

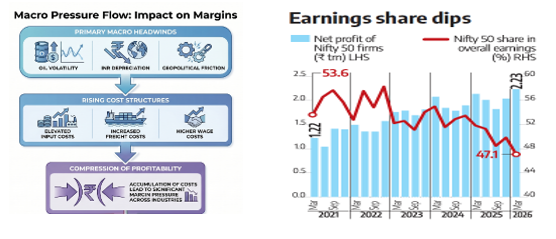

As stated before in earlier monthly reports, every USD 10/barrel increase in crude oil prices pushes headline inflation up by 40- 60 basis points while reducing GDP growth by 20 to 40 basis points. And these are 1st order impacts, the second order impact is even more and CPI inflation could increase by 80-100 bps (much of it will be pass through Wage-price loops and freight/logistics) and GDP could decline by ~60 bps. Companies have the hardest job at hand and they will have to juggle between price hike vs absorption so has to maintain a balance between demand impact and their own margin impact. Clearly, how much they absorb and pass on, will guide for CPI inflation ahead. Just for the data itself, WPI jumped to 8.30% in April from just 2.13% in February. Majority of the impact has also been reflected by the rupee which has depreciated to levels near 96/USD. Clearly, ~6% YTD depreciation in rupee is a loss for a foreign investor considering that the stock has remained rock solid.

To make matters worse, India taxes capital gains at the source vs other countries, a pain point which has been highlighted by foreign investors as a major sore one. Recently, they have been removed for G-Secs but not so far for equities. The RBI in its latest monetary policy has kept repo rates on hold at 5.25% however, revised FY27 CPI forecast to 5.1% (vs 4.6% earlier) and lowered GDP forecast to 6.6% (from 6.9% earlier). The RBI has also taken measures to attract foreign capital which might support rupee ahead.

Source: Notebook LM and Business Standard

Unfortunately, FIIs are not going to return anytime soon to equity markets unless the problems plaguing the country disappears overnight. However, the relative attractiveness for India also hinges upon the narrative over AI capex and whether it's in a bubble and when it's going to burst. Clearly, the equity markets in Korea and Taiwan have witnessed very truncated rally driven by the AI theme and that could burst. India could be back in focus with the rupee already depreciated, manufacturing and exports could support massively. Besides, the government has also actively focused on building India's defence sector. We believe, domestic consumption and banking sector will find its challenges while defence manufacturing, electrification led demand for power equipment together with focus on indigenisation theme will play out strongly across many sectors, along with self-reliance in critical minerals. Unfortunately, India's benchmarks represent yesterday's winners and hence, the rupee depreciation benefits will not be captured well. In fact, a recent Business Standard article shared that the share of Nifty 50 companies in the combined adjusted net profit of all listed firms fell to 47.1% in Q4FY26, down from 51.8% in Q4FY25 and 49.8% in Q3FY26. This is just the proof that Nifty 50 is losing the relevance and failing to capture the India earnings story. Nifty 500 companies have witnessed higher revenue/EBITDA/PAT growth vs Nifty 50 companies. The Nifty 50 FY27 earnings forecast has been revised lower by 9%. According to a Moneycontrol article, 31 of the 50 Nifty constituents (61% of the index) suffered FY27 earnings downgrades in May alone. Thus clearly, the growth opportunities are not exactly captured by the benchmarks. Rupee depreciation while highlights our external vulnerabilities, it does make our exports competitive - INR has also depreciated by ~20% against Chinese yuan in last 1 year. With anti-involution in China and moving to value added products, it does open up opportunities for India, unfortunately not captured by benchmarks.

Macro Overview & Outlook

The broader macro-economic outlook still remains affected by the West Asian War which is still far from coming to any meaningful conclusion. Several attempts at reaching a consensual decision regarding peace, policies and mutual cooperation. A decisive outcome in unlikely in the near future.

Internally, the domestic investors and other market participants will look forward to the MCP's decision regarding key policy rates. Given the geopolitical instabilities, we expect RBI to remain cautious and do not expect any changes in policy rates. Inflation is likely to rise due to rise in fuel prices.

Coming to this month's theme - the world needs significant capital investment over the next decade and a half for maintaining and upgrading the legacy infrastructure while it continues to develop new infrastructure projects such as data centers. The "Three D" megatrends of digitalization, decarbonization and deglobalization will continue irrespective of the political environment. Towards this end two major sectors that are getting boosted through favourable policy push are defence and power. This is in line with the government's stated objectives of indigenization and achieving self-reliance in manufacturing. But manufacturing and infrastructure growth both needs massive power supply. As of early 2026, India's overall installed power capacity crossed 520 GW, with non-fossil fuel sources accounting for over 52% of the total.

India is rapidly advancing toward complete self-sufficiency in both its power and defence sectors through aggressive domestic manufacturing policies, sweeping financial reforms, and a strategic pivot away from foreign imports. Driven by the Make in India initiative and the Atmanirbhar Bharat Abhiyan (Self-Reliant India Mission), the country is transforming itself from a historic importer into an agile global powerhouse across both domains.

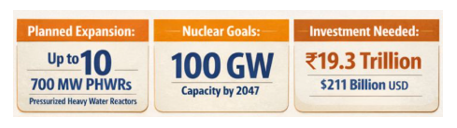

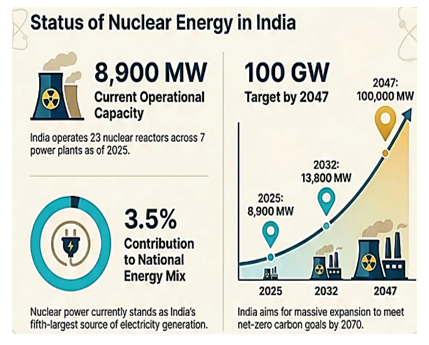

The GoI is executing a major strategic shift to achieve power security, backed by a target of 100 GW of nuclear capacity by 2047. While currently providing a modest ~8.8 GW and ~3% of the generation mix, the sector is scaling rapidly through massive investments, domestic technology development, and private sector participation.

Nuclear Power - Emerging Growth Story

India has set a target to achieve 100 GW of nuclear power capacity by 2047, over tenfold increase from its present capacity of ~8.8 GW. This ambition is central to GoI's "Viksit Bharat @2047" vision and the broader commitment to reach net-zero emissions by 2070. Domestic nuclear energy market was valued at ~$927 mn in 2024. India currently operates 25 reactors. To meet the massive 100 GW requirement an estimated ₹15–18 lakh crore of investments would be required. This massive funding requirement has urged GoI to open up the sector to private and foreign participation.

The Sustainable Harnessing and Advancement of Nuclear Energy for Transforming India (SHANTI) Act, 2025, was enacted to resolve long-standing civil liability issues, facilitating international collaboration and private investment. Favourable Land Acquisition rules allows "in-principle" agreements to reduce "exclusion zones" around plants by 50% for large reactors and nearly 2/3rd for small units to free up land for expansion.

A key growth driver is entry of private sector. Major players like Adani Power and NTPC are already entering. Adani has established subsidiaries for nuclear projects, while NTPC is conducting feasibility studies for plants in 14 states. NTPC is aggressively pivoting toward nuclear energy, aiming to capture a 30% market share of India's planned 100 GW nuclear capacity by 2047. As part of this, the state-owned power giant is targeting the development of 30 GW of nuclear capacity over the next two decades.

Stock Recommendations

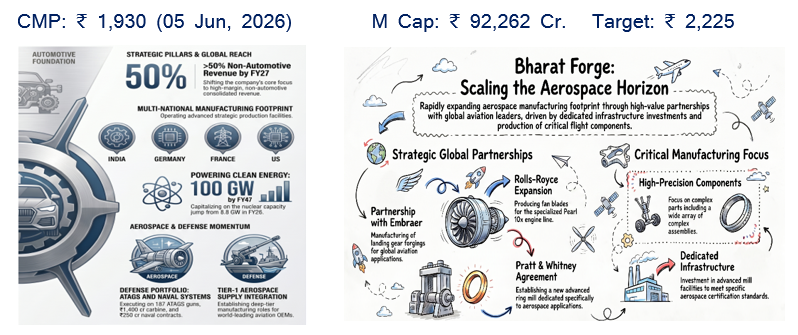

- Bharat Forge Ltd.

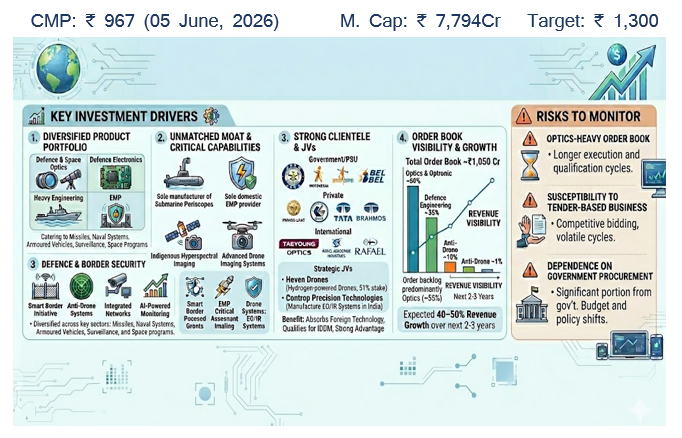

- Paras Defence and Space Technologies Ltd.

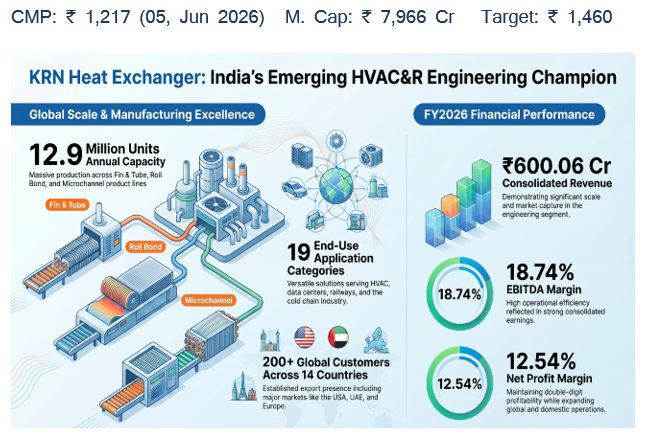

- KRN Heat Exchanger and Refrigeration Ltd.

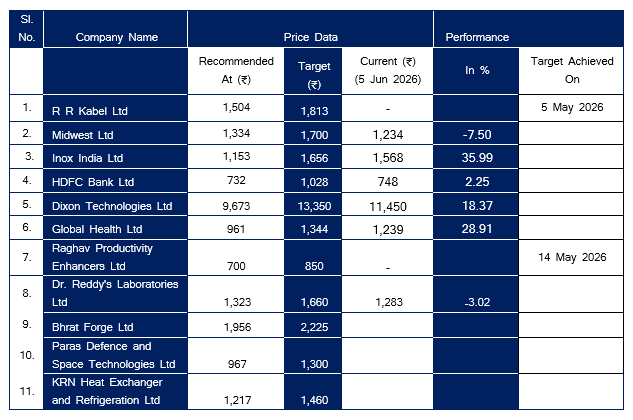

Performance Radar

Research Team

Partha Mazumder (partha@easternfin.com)

Sanjukta Majumdar (research@easternfin.com)

Sayantina Mallick Chowdhury (sayantina@easternfin.com)

Disclaimer

Eastern Financiers Limited (hereinafter referred to as ‘EFL') (RA Registration No: INH000022756, Type: Non-Individual) is a Member registered with SEBI having membership of NSE, BSE, MCX. It is also registered as a Depository Participant with NSDL. It is also having AMFI certificate for Mutual Fund Distribution. The associate of EFL is engaged in activities relating to Insurance Broking. No disciplinary action has been taken against EFL by any of the regulatory authorities. EFL/its associates/research analysts do not have any financial interest/beneficial interest of more than one percent/material conflict of interest in the subject company(s). EFL/its associates/research analysts have not received any compensation from the subject company(s) during the past twelve months. EFL/its research analysts have not served as an officer, director or employee of company covered by analysts and has not been engaged in market making activity of the company covered by analysts. This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision.

Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and risks of such an investment. Reports based on technical and derivative analysis centre on studying charts of a stock's price movement, outstanding positions and trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals. The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for general guidance only. EFL or any of its affiliates/group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. EFL has not independently verified the information contained within this document. Accordingly, we cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While EFL endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory compliance or other reasons that prevent us from doing so. The report is for information and education purposes only. It must not be construed as any solicitation of any investment or any BUY/ SELL/ HOLD recommendation. Investments are subject to market risk. The user must do his/ her own research before taking any investment decision. Eastern Financier Limited is not liable for any consequence of any action taken by the user on the basis of this report.

Register on SCORES Portal LEDO

Register on SCORES Portal LEDO