Market Overview & Outlook

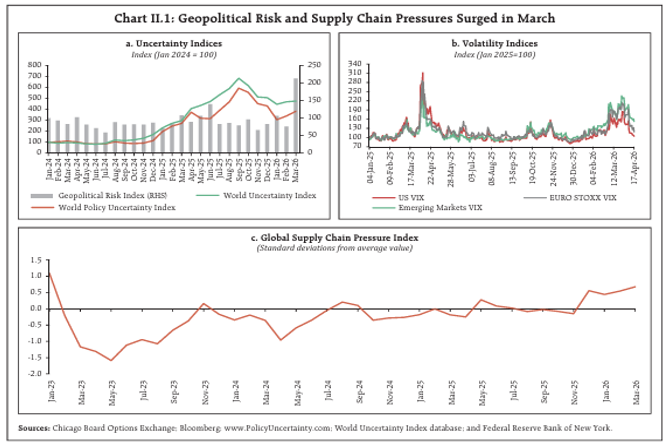

Global equity markets haven't shown signs of concerns even though the global macro set up remains grim. Outperformances in US, Korea and Taiwan markets have been linked with the AI/Semiconductor stocks. Nonetheless, Brent crude prices are now hovering above USD 113 per barrel and the Strait of Hormuz showing no signs of opening. There are couple of possibilities that either the global markets are underestimating the risks ahead (and would eventually adjust) while betting the shocks to be temporary in nature and the "TACO" trade is alive (assuming the economic pain will eventually be sustainable thus warranting de-escalation). However, that does depend on the negotiations between Iran's leaders and the US, albeit Iranians don't want to make much concessions on Nuclear Programme, a sore point to start with.

Source: Financial Times

According to a Financial Times article by Mr. Martin Wolf, who highlights the importance of Strait of Hormuz and it's not just crude oil, as 50% of world's seaborne trade in sulphur, 19% of refined oil products, 29% of LPG and 19% of LNG, 13% of chemicals (including fertilizers), crucial metal like aluminium, all passes through the Strait of Hormuz. He further highlighted from "The World Bank's Commodity Markets Outlook", wherein the initial impact of global loss of 10.1 million barrels per day of oil in March was higher than major events earlier, which impacted oil flows. The World Bank further states that out of the total loss of 20 million barrels per day, about 1.5 million could be offset by other OPEC producers, 5.5 million through alternative pipelines, 3.3 million from existing inventories, 3.9 million from sanctioned oil already in transit, 0.5 million from increased output in high-income countries, and another 0.5 million from biofuels (though this is harder now due to fertiliser shortages). Even after these adjustments, a deficit of 4.6 million barrels per day remains, which is just over 4% of global consumption and could reach to potentially 8%, when inventories run dry.

Now clearly how long does the closure of Strait of Hormuz last and again how long does it take for things to normalize. World Bank does estimate that the worst of the supply disruptions to subside by May. Afterward, traffic through the strait is likely to recover slowly, eventually returning to near pre-war levels by Q4 of CY2026. Under these assumptions, the bank projects its energy price index will climb 24% over the year. Fertiliser prices are anticipated to rise by 31%, with urea jumping as much as 60%, while food prices are predicted to increase only modestly-by about 2% (given the large stocks in hand). While India imports 85-86% of its crude oil and 60% of LPG requirements. In Urea, India's dependence has decreased over the last decade, but still imports 25-30% of its requirements while for non-urea fertilizers- specifically DAP (Di-Ammonium Phosphate), MOP (Muriate of Potash), and NPK complexes-the import share is at 60-65%, 100% and 20-25% respectively.

The rising prices will put pressure on Govt's subsidy burden especially for Urea whose prices are capped at ₹242 per 45 kg bag while for non-urea fertilizers, the prices are not fixed but monitored. The Government has already stretched the subsidy burden due to rising gas costs (for Urea production) while for the imports, it will be much higher. Thankfully, the pain will not be felt this year due to thrice the buffer stock of wheat and rice than stipulated, however, it will raise production costs, which will be felt next year.

To make matters worse, IMD has projected southwest monsoon rainfall at 92% of the Long Period Average (LPA) together with likely emergence of El Nino conditions. Thus, there could be double impact of higher input costs and lower production, thus raising food inflation (46% of India's CPI basket). Every USD 10 per barrel hike in crude raises CPI inflation by ~60bps. Assuming, crude averages ~USD 90 per barrel, and taking Feb 2026 inflation (of 3.21%) as starting point, it could add ~180 bps to CPI inflation, thus reaching a figure ~5%, just accounting for crude only. RBI's task would be challenging but rate hikes would likely be discounted ahead while risks of higher fiscal deficit could crowd out private investment. Clearly these are the risks which have kept Indian equity markets on tenterhooks as valuation might further come down and the rupee has borne the brunt. The recent high frequency indicators like IIP, PMI have also showed challenges while CPI inflation has inched, petrol and diesel prices are yet to be hiked while WPI spike (3.88% in Mar'26 vs 2.13% in Feb'26) captures the picture.

Source: https://metalsandminers.substack.com/

One of the positive factors which has supported US equity indices is strong corporate earnings. For India as well, the early bird companies in Q4FY26 (January–March 2026) reported encouraging earnings despite headwinds from the war in West Asia, with banks, non-bank lenders, and metal producers like Hindustan Zinc providing a boost, reports a Business Standard article. Combined adjusted net profits of 141 companies rose 14% year-on-year - the fastest pace in 10 quarters - reaching around ₹1.28 trillion, up from ₹1.12 trillion in Q4FY25. Excluding BFSI and oil & gas, earnings growth was the best in 16 quarters, with combined adjusted net profits up 19.7%. More importantly, combined net sales rose 9.2% YoY - the fastest in seven quarters - driven partly by higher commodity and energy prices stemming from the West Asia conflict. EBITDA margins improved ~30 basis points YoY and ~200 bps quarter-on-quarter to 35.2% of total income, aided by moderation in salary and overhead costs. Going ahead, however, there risks of EBITDA margin compression as producers may not be able to pass on the higher input costs. Earnings growth estimates for FY27 has started getting revised lower from 10-12% vs 6-10% now. Nifty EPS thus is trading at P/E of ~19x FY27E EPS, which is not cheap by any chance.

One of the substack articles (https://metalsandminers.substack.com/) highlighted that even in 1973 oil embargo, the stock market didn't go through the correction while the embargo was active, but in six months after the embargo was lifted. Capital moved to safe haven assets like gold. While history doesn't repeat itself, it certainly does rhyme. Probably global markets are complacent for the time being, we would know in six months or so, after the Strait of Hormuz reopens. It is thus advisable not to invest heavily at this point but to keep the powder dry as we might get better opportunity ahead.

Macro Overview & Outlook

"The conflict in West Asia has intensified pressures on the global supply chains in March with some easing observed in the first half of April. Domestic economic activity displayed resilience in many segments with slowdown in a few others. CPI inflation, driven by fuel and food, marginally edged up in March. The money market and bond yields moderated after the temporary ceasefire in West Asia. A slowdown in imports and expansion in exports narrowed trade deficit to a nine-month low. Foreign portfolio investment (FPI) flows remained volatile, although net foreign direct investment (FDI) turned positive in February" (RBI Bulletin April 2026).

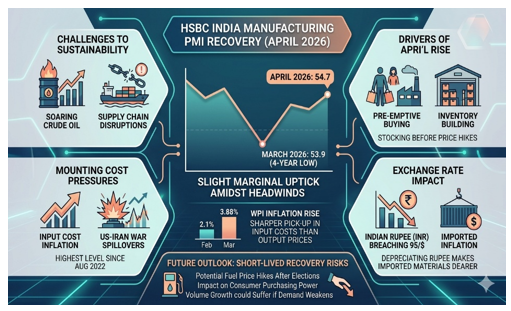

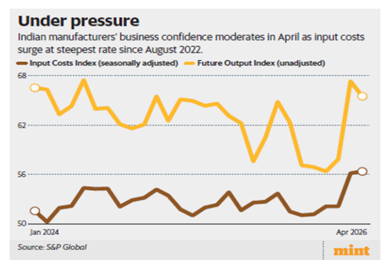

India's manufacturing sector experienced a significant surge in cost pressures in April 2026, with input costs rising at their fastest rate since August 2022. While the headline HSBC India Manufacturing PMI (compiled by S&P Global) rose slightly to 54.7 from a four-year low of 53.9 in March, overall business confidence moderated. The marginal recovery seen in India's Manufacturing Purchasing Managers' Index (PMI) for April 2026 is most likely to be temporary due to underlying economic pressures. While the index rose to 54.7 in April 2026 from a four-year low of 53.9 in March, current data suggests this momentum could fade.

The manufacturers remain generally optimistic about growth prospects. However, the overall level of positive sentiment slipped in April compared to March. Which raises the question as to whether the recovery will sustain. Confidence is currently tied to successful marketing efforts and the anticipated clearance of pending projects. Early signs of deceleration are now becoming more apparent when we look at certain indicators like port cargo, air passenger traffic and the outlook of purchasing managers. The manufacturing PMI, albeit in expansionary zone (above the 50 mark – which testifies resilience), is near its lowest level in nearly four years.

Cost Inflation and Margin Pressures continue to weigh heavily.

Rapid Surge: Input cost inflation reached a 44-month high. Manufacturers reported higher prices for critical materials, including aluminum, fuel, chemicals, and rubber, largely attributed to the ongoing Middle East conflict.

Price Pass-Through: To protect margins, goods producers raised their selling prices at the sharpest rate in six months.

Wholesale Price Index (WPI): Earlier data from March showed WPI inflation hitting a multi-month high of 3.88% in March (April numbers are awaited), reflecting a sharper pick-up in input costs compared to output prices.

An emerging area of interest is AI, and its application in finance. Artificial Intelligence has started reshaping the ways in which "financial institutions serve customers, process documents, assess credit, monitor risks, and strengthen oversight". The transition is happening at a remarkable speed. Finance will definitely become more intelligent. But question arises as to whether finance will continue to remain fair, accountable, humane and most importantly inclusive (a key pillar for India's economic wellbeing and progress).

Finance is overwhelming, documentation-heavy, language-bound, and quite frequently, in modern world, is physically distant. In a country as large and diverse as India, technology can help reduce several of these frictions. AI can make financial services more inclusive, efficient, and secure in the following ways.

Accessibility: Using multilingual chatbots and voice interfaces to overcome language and paperwork barriers.

Credit Inclusion: Supplementing traditional credit scores with AI-driven insights to help small businesses and first-time borrowers.

Security: Improving fraud detection by identifying suspicious patterns in real-time within payment systems.

Supervision: Using intelligent tools to manage risk and provide early warnings for financial institutions and regulators.

Concern: AI in finance offers significant potential for enhancing financial inclusion and fraud detection, yet it simultaneously introduces risks regarding algorithmic bias, data privacy, and systemic vulnerability. To ensure safety and accountability, the adoption of these technologies requires robust transparency and governance frameworks. Proper regulatory framework is yet to develop but is immensely important for AI application.

The road ahead: Five core principles for responsible AI adoption in finance include maintaining human accountability, ensuring fairness and explainability, implementing strict data governance, strengthening institutional capacity, and prioritizing inclusive design. These principles emphasize that AI should serve, rather than exclude, marginalized users while keeping human judgment central to decision-making. Read the full guidance at the Reserve Bank of India website.

Stock Recommendations

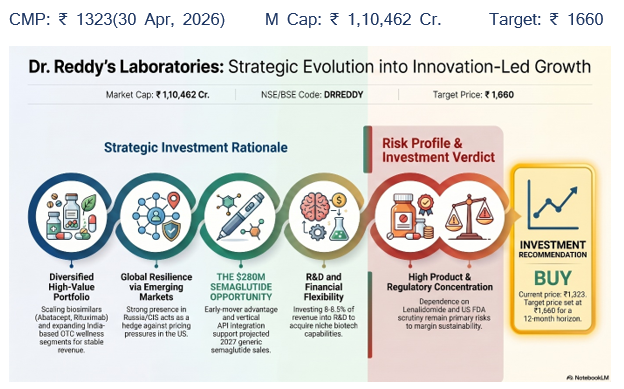

- Dr Reddy's Ltd.

Click here to know more

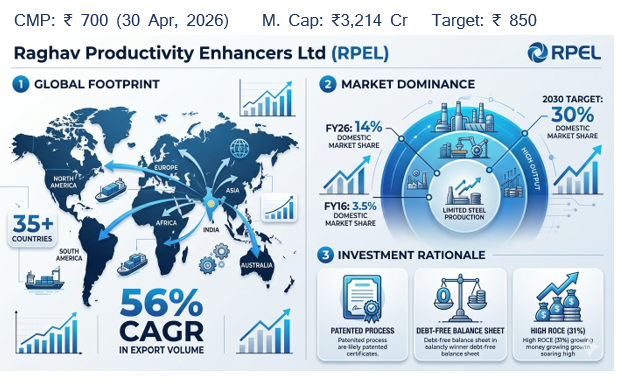

- Raghav Productivity Enhancers Ltd.

Click here to know more

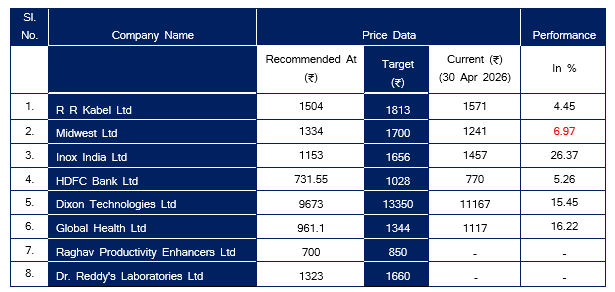

Performance Radar

Research Team

Partha Mazumder (partha@easternfin.com)

Sanjukta Majumdar (research@easternfin.com)

Sayantina Mallick Chowdhury (sayantina@easternfin.com)

Disclaimer

Eastern Financiers Limited (hereinafter referred to as ‘EFL') (RA Registration No: INH000022756, Type: Non-Individual) is a Member registered with SEBI having membership of NSE, BSE, MCX. It is also registered as a Depository Participant with NSDL. It is also having AMFI certificate for Mutual Fund Distribution. The associate of EFL is engaged in activities relating to Insurance Broking. No disciplinary action has been taken against EFL by any of the regulatory authorities. EFL/its associates/research analysts do not have any financial interest/beneficial interest of more than one percent/material conflict of interest in the subject company(s). EFL/its associates/research analysts have not received any compensation from the subject company(s) during the past twelve months. EFL/its research analysts have not served as an officer, director or employee of company covered by analysts and has not been engaged in market making activity of the company covered by analysts. This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment decision.

Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and risks of such an investment. Reports based on technical and derivative analysis centre on studying charts of a stock's price movement, outstanding positions and trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamentals. The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for general guidance only. EFL or any of its affiliates/group companies shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. EFL has not independently verified the information contained within this document. Accordingly, we cannot testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While EFL endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory compliance or other reasons that prevent us from doing so. The report is for information and education purposes only. It must not be construed as any solicitation of any investment or any BUY/ SELL/ HOLD recommendation. Investments are subject to market risk. The user must do his/ her own research before taking any investment decision. Eastern Financier Limited is not liable for any consequence of any action taken by the user on the basis of this report.

Register on SCORES Portal LEDO

Register on SCORES Portal LEDO